Your treasurer just pulled cash balances from four custodian portals, dropped them into a spreadsheet, and reconciled them against last week's wire activity. By the time that view is usable, it's already a few days old. And it still doesn't tell you whether next month's capital calls will clear without selling something.

That's the problem with the basic cash tracking that most family offices use. Cash makes up about 8% of the average portfolio (UBS Global Family Office Report 2025), but it funds every distribution, every call, and every tax bill that flows out of the office.

Most wealth platforms piece together data after the fact in order to convey what happened. They rarely tell you what's coming next or what your idle balances are quietly costing you.

This guide breaks family office cash flow into specific reports, what each one actually answers, and how a consolidated view turns thousands of transactions across custodians, entities, and currencies into one forward-looking picture.

Key Takeaways

What is family office cash flow tracking, and why is it different?

Family office cash flow tracking is the discipline of recording, consolidating, and projecting every movement of cash across all accounts, custodians, entities, and currencies. It differs from corporate cash management because family office portfolios span operating cash, marketable securities, and illiquid private-market commitments at the same time. Those commitments draw and return cash on schedules that a bank statement never shows.

A useful way to think about cash flow is as three separate reporting layers:

- Actuals: what has already moved through the accounts.

- Projection: what is expected to move over the coming months.

- Cost: what the portfolio pays out in fees, commissions, and advisory charges to operate.

Most teams collapse all three into a single spreadsheet tab, which is precisely why the view breaks the moment a second currency or a third custodian enters the picture.

Cash flow tracking is also distinct from liquidity reporting. Liquidity reporting measures whether the family can meet obligations: coverage ratios, days-to-cash, tiered reserves. Cash flow tracking is the underlying record that feeds those metrics: the transactions, projections, and costs that fuel a liquidity analysis.

For the measurement side, see our companion guide on liquidity vs. performance.

Why is cash flow harder to track in a family office?

Cash flow is hard to track in a family office because cash enters and leaves through multiple custodians, entities, and currencies at once.

At the same time, illiquid investments generate capital calls and distributions that arrive off-schedule and never appear on an ordinary bank statement. Alternatives now represent 42% of family office portfolios, up 3% from the prior year (BlackRock 2025 Global Family Office Survey). Every alternative investment creates a sequence of future cash events with uncertain timing.

Four operating realities make the cash side uniquely difficult.

- Cash is held with dozens of custodians, each with its own statement format and timing.

- Private-market commitments draw capital early and distribute late, so the office is often cash-flow-negative on a position for years before it turns.

- The structure is multi-entity and multi-currency (operating companies, trusts, holding LLCs, foundations, and personal accounts, often across three to seven currencies), with intercompany movement that risk distorting any consolidated view.

- Income frequently arrives net of items a raw feed obscures, such as non-resident alien (NRA) tax withholding on a dividend, or a deposit-sweep interest credit that looks like noise until you reconcile it.

The practical result is that the “cash balance” a principal sees is often a sum of stale, inconsistent numbers. Reconciling them to one figure that can be trusted, and then decomposing that figure back to the entity and custodian levels that the controller needs, is the core challenge in cash flow reporting today.

The cash flow reports every family office needs

A complete cash picture only requires a small library of reports. They group into the three layers introduced above:

- “actuals reports” answer what moved.

- “projection reports” answer what is coming.

- “cost reports” answer what it took.

Running them together is what converts raw activity into decisions. This matters because internal expertise gaps were cited as the top challenge related to technology adoption for family offices (Citi 2025). When expertise levels are mixed, the unstructured, one-tab approach is often less reliable compared to one-at-a-time report generation.

The actuals layer typically includes a combined transaction and cash flow ledger, a focused cash flow report, a running-balance cash ledger, a transfers in/out report, and an income report.

The projection layer adds a cash projection summary (category-level) and a cash projection detailed report (per security).

The cost layer adds a trade-commission-and-account-fees summary by custodian and a consolidated commissions, account, and advisory fees report.

The sections below walk through the three layers in turn. The point is not that a family office should produce 10 reports for their own sake. It’s that every cash-flow question a principal or controller might ask is capably answered by a specific report.

Trying to answer every question from one view is where cash flow frequently breaks down. Instead, map every given report onto one of the layers above while making sure the layers themselves share a trusted data layer.

Reporting on actual cash flow: transactions, the cash flow report, and the cash ledger

The actuals layer answers two questions: what actually moved, and what is my real, reconciled balance. Three reports do most of the work, and each has a distinct job. Getting this layer right is foundational, and even small classification errors here distort the entire liquidity view that sits above it.

Transactions and the transaction & cash flow report

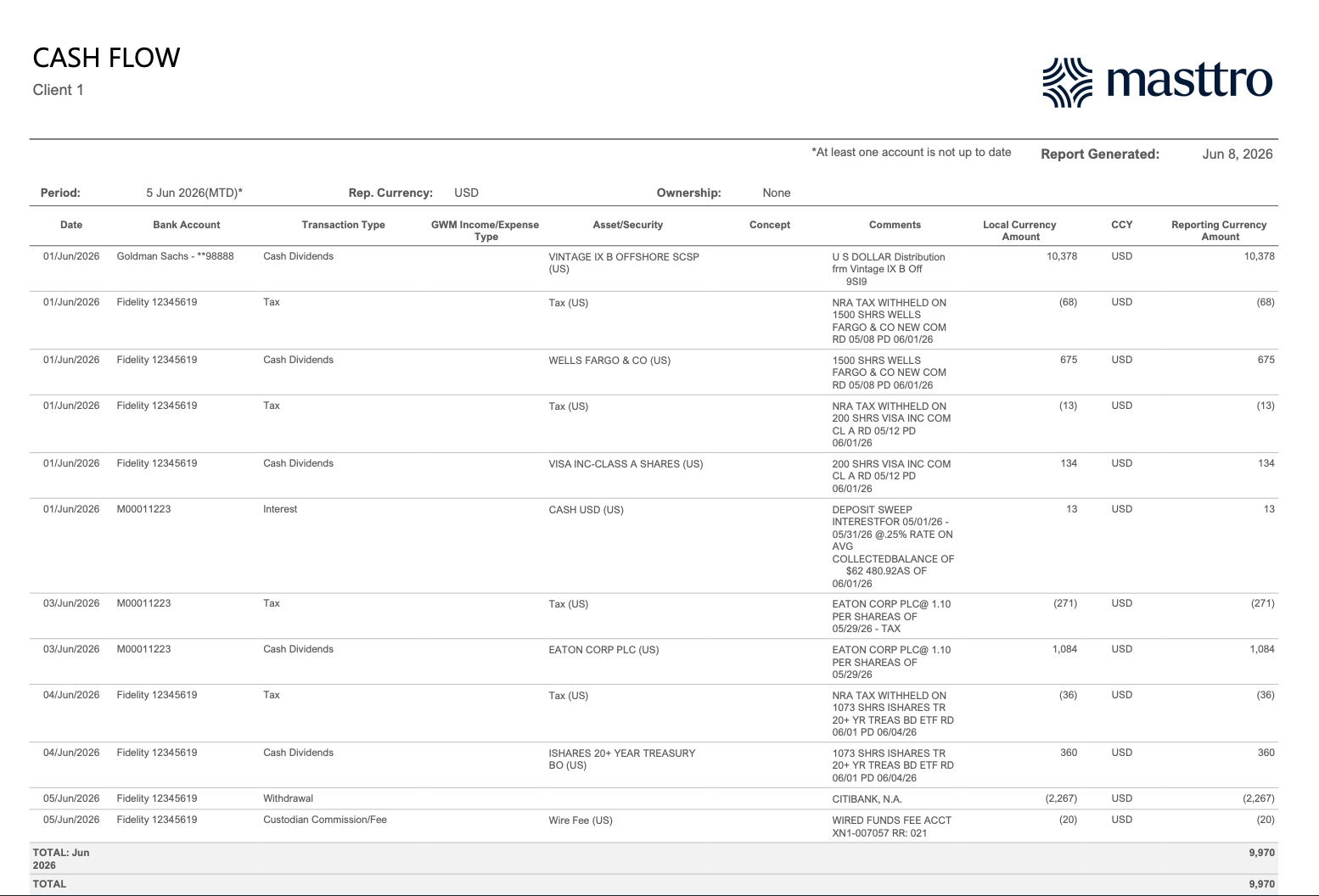

A combined transaction and cash flow report is the most complete single view of activity. It lists every cash-affecting event (buys, sells, capital calls, dividends, interest, tax, and fees) with quantity and net price for trades, amount-only lines for calls and income, and both local and reporting currency for each row.

A separate transactions report narrows the same data to capital-related activity (capital calls, buys, sells) with contract numbers, which is what the controller needs when reconciling a specific commitment. That means recognizing that a single day can contain a $55,000 capital call, a $10,000 fund distribution, and a $675 dividend booked net of NRA tax withholding. The report recognizes three discrete cash events that a raw bank feed would flatten into noise.

The cash flow report

The cash flow report narrows the lens to income, expense, and deposit/withdrawal activity, with a clear period total. It answers a more granular question: what was my net operating cash movement this period, without the position-change noise of the full transaction ledger.

Dividends, interest, tax, withdrawals, and custodian wire fees all land in this report, netting to a single month-to-date figure that a controller can tie out. It complements the full ledger rather than duplicating it: one shows everything, the other isolates the cash that actually changed the bank balance.

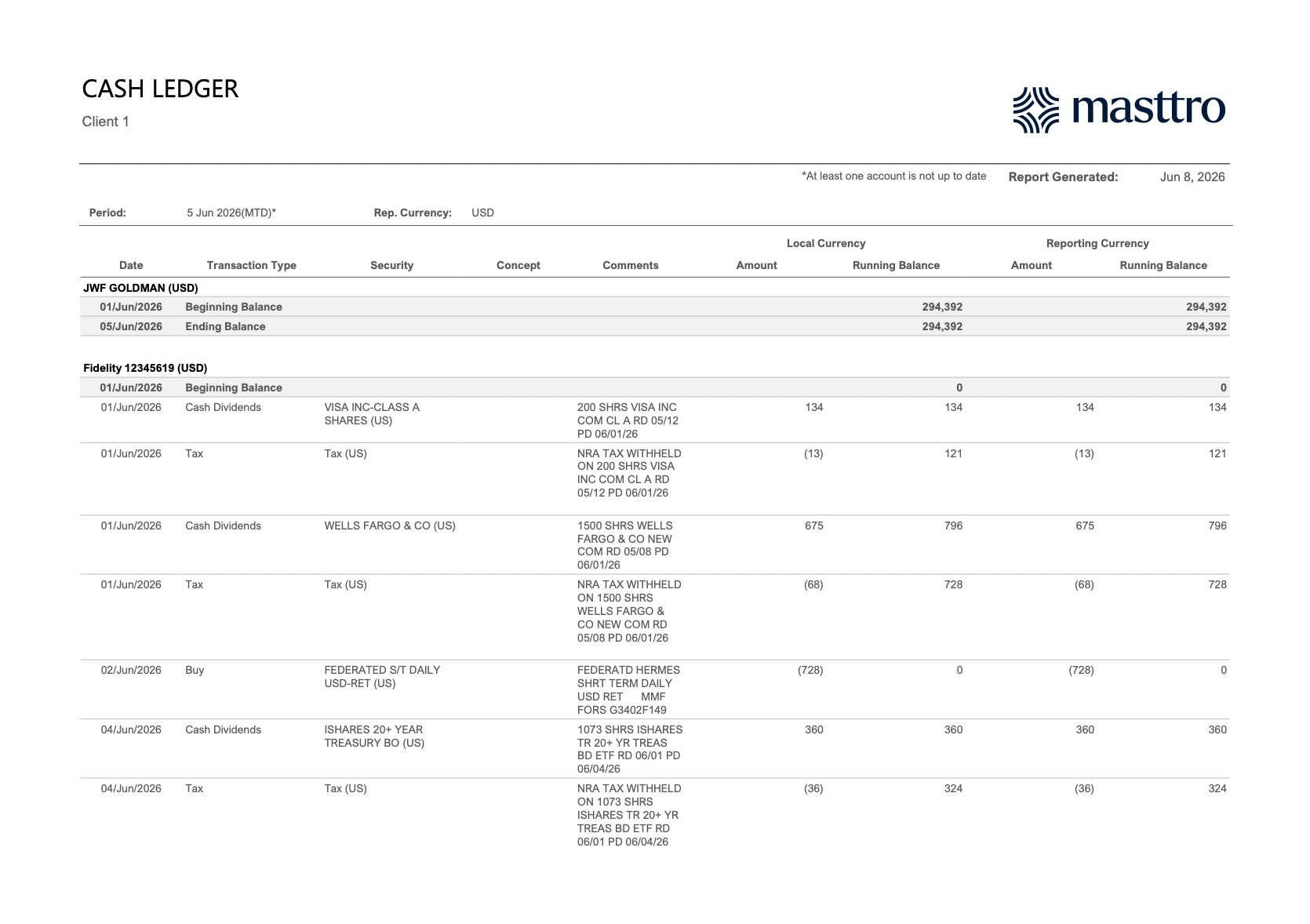

The cash ledger and running balances

The cash ledger is the reconciliation backbone. It shows a beginning and ending balance per account, with a running balance after each transaction, in both local and reporting currency. This is the report that proves the consolidated cash number is right, line by line.

With 48% of family offices naming liquidity improvement as their top investment objective for 2026 (RBC/Campden, October 2025), an audit-ready running balance is a valuable trust layer beneath every projection and every decision. If the actuals do not reconcile, nothing downstream can be relied on.

How do you project future cash flow and capital calls?

Forward cash projection answers the question that keeps controllers up at night: will I have enough cash, and when?

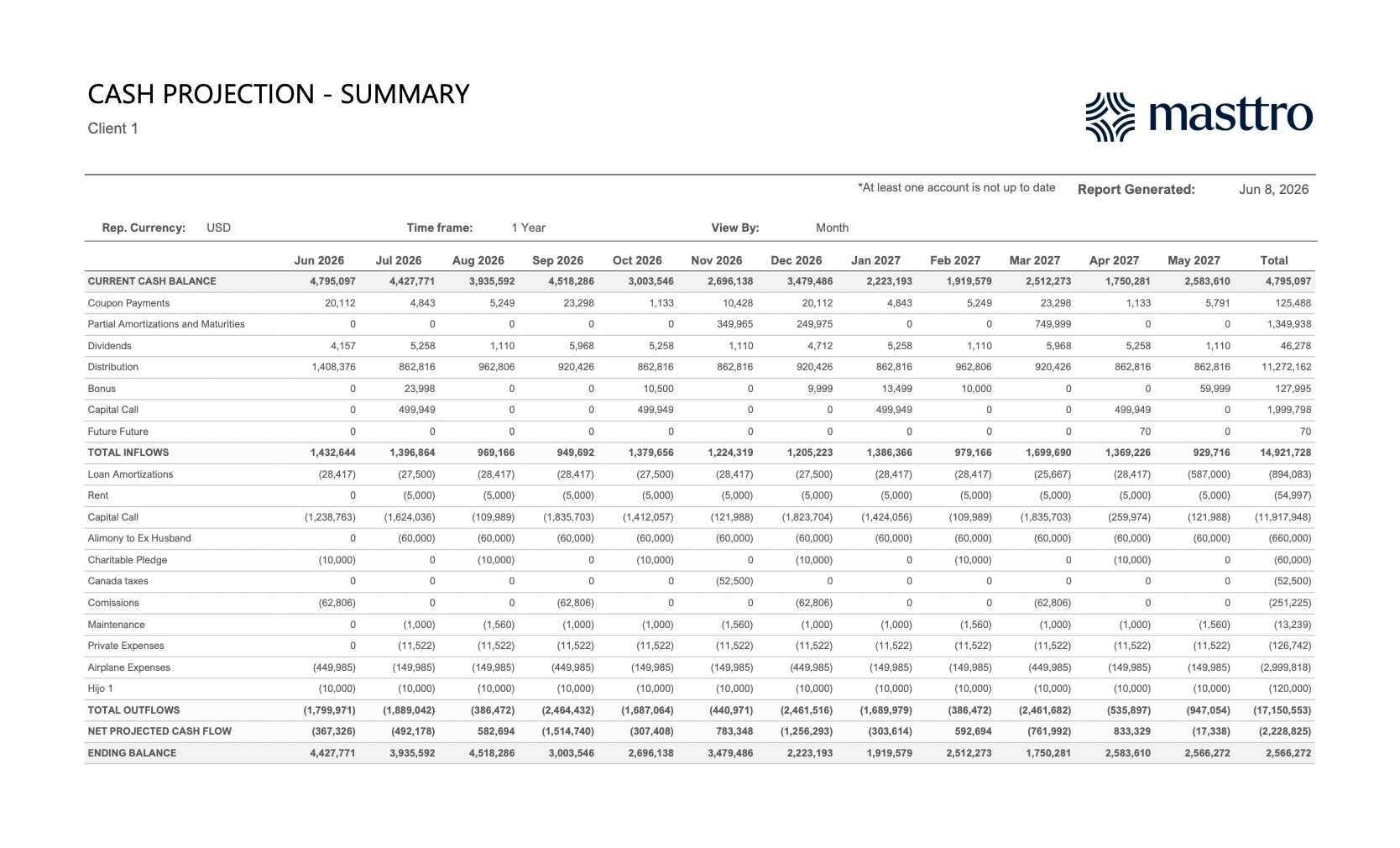

The report models expected inflows (coupon payments, dividends, bond maturities and amortizations, and fund distributions) against expected outflows (capital calls, loan amortizations, rent, and operating and lifestyle expenses) across a rolling 12-month horizon, surfacing the net projected cash flow and ending balance for each month.

With private market investments comprising 29% of the average family office portfolio (RBC/Campden, October 2025), the future capital-call load is rising, and projecting its timing is key to both managing liquidity risk and finding market opportunities.

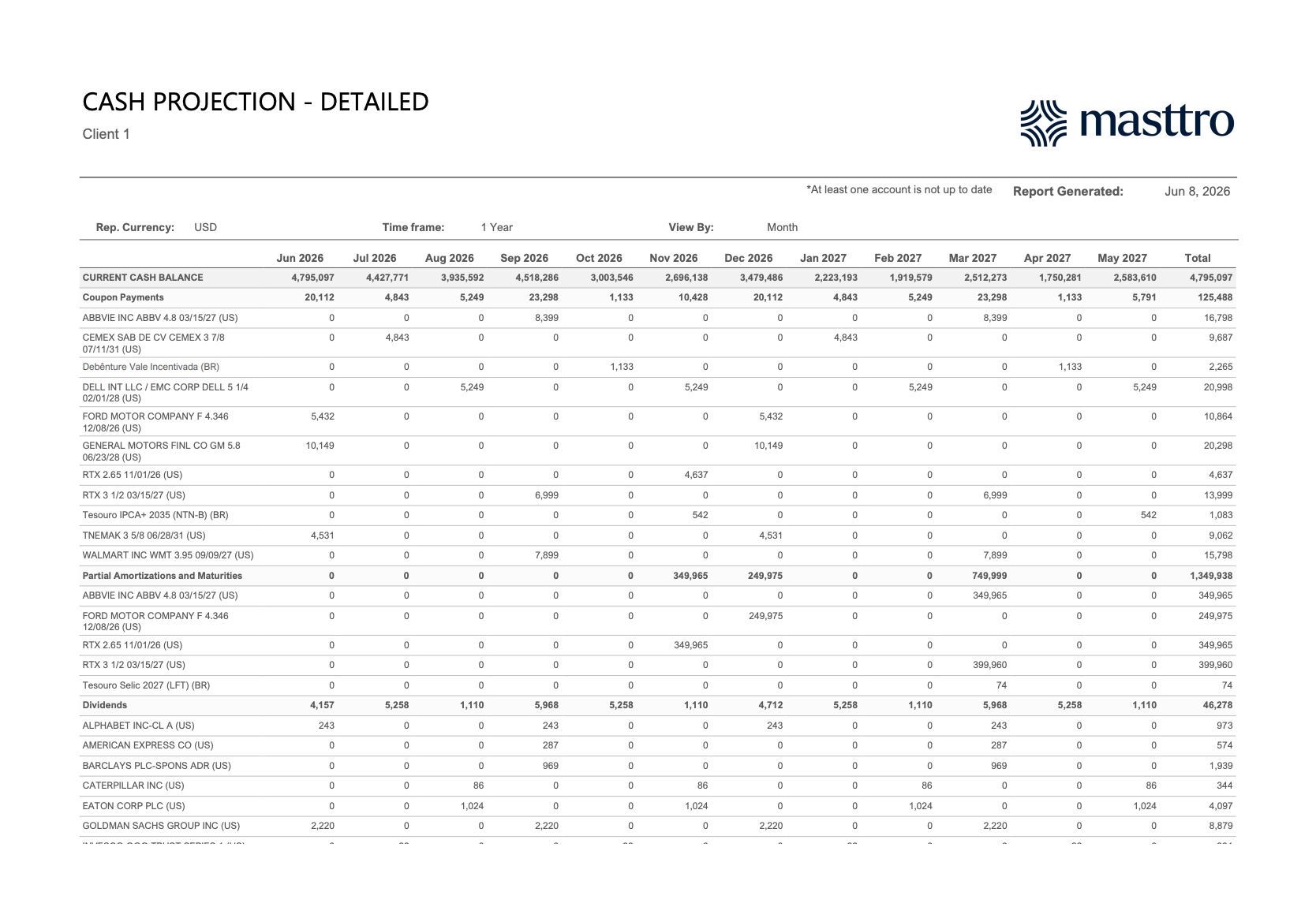

Two reports cover this in practice. A cash projection summary shows the picture at the category level: total inflows, total outflows, net projected cash flow, and ending balance month by month. A cash projection detailed report breaks the same horizon down per security, so the controller can see exactly which bond pays a coupon in September or which holding amortizes in March.

The summary is what the principal reviews; the detail is what the analyst builds it from.

The trickiest input is the capital call. Notices typically arrive on only a few business days’ notice, and a single call can draw a large share of a commitment at once, with little warning.

A credible projection therefore reserves cash against probability-weighted future calls. It also stress-tests the ending balance against an early or outsized call, so the office knows in advance whether it would fund from cash, from a credit line, or by trimming a liquid position.

For the mechanics of handling the notices themselves, see capital call processing for family offices and the broader workflow in alternative investment reporting for family offices.

Alternatives Reporting: From Below the Line to All of the Above

The cost side: fees, commissions, and advisory charges

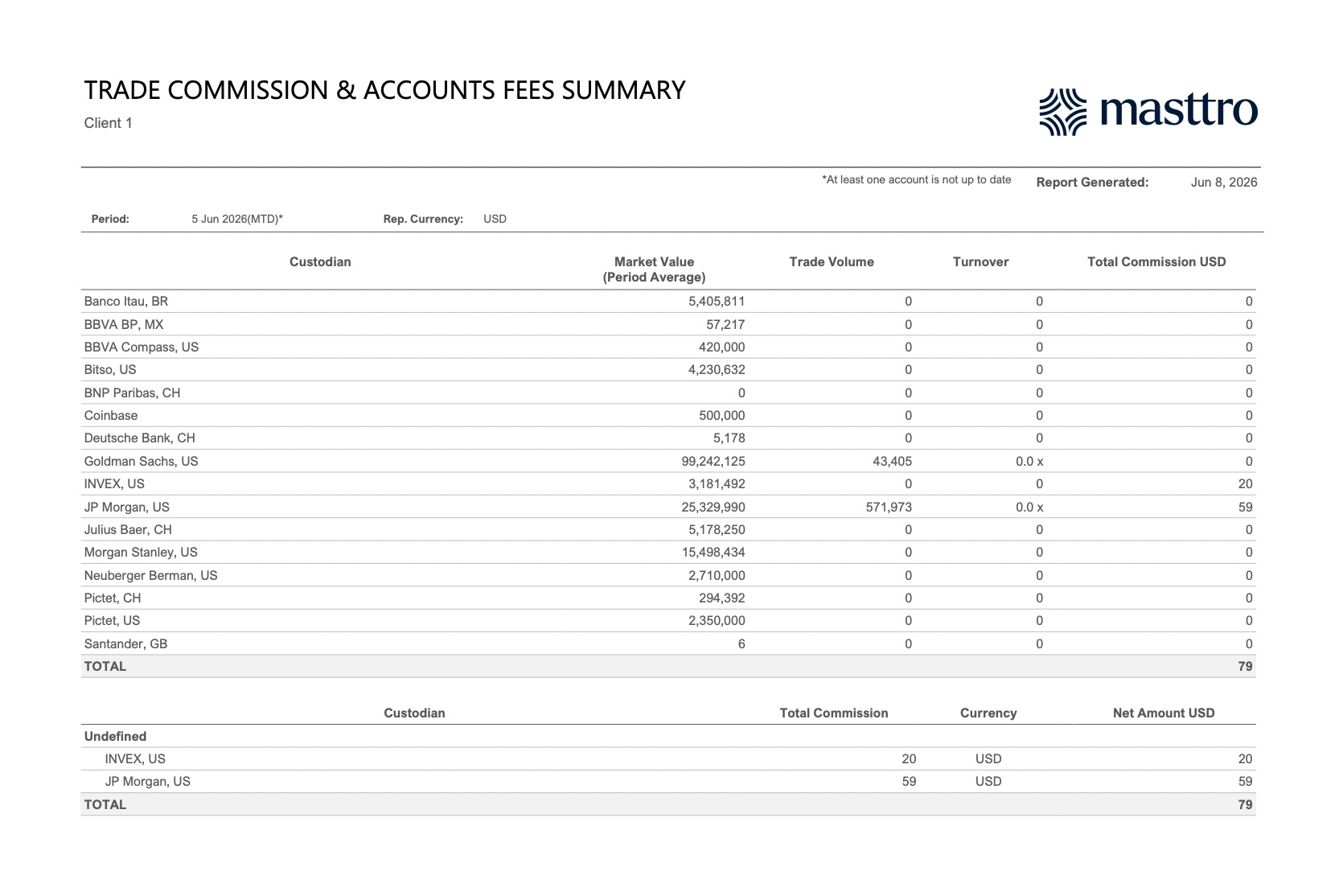

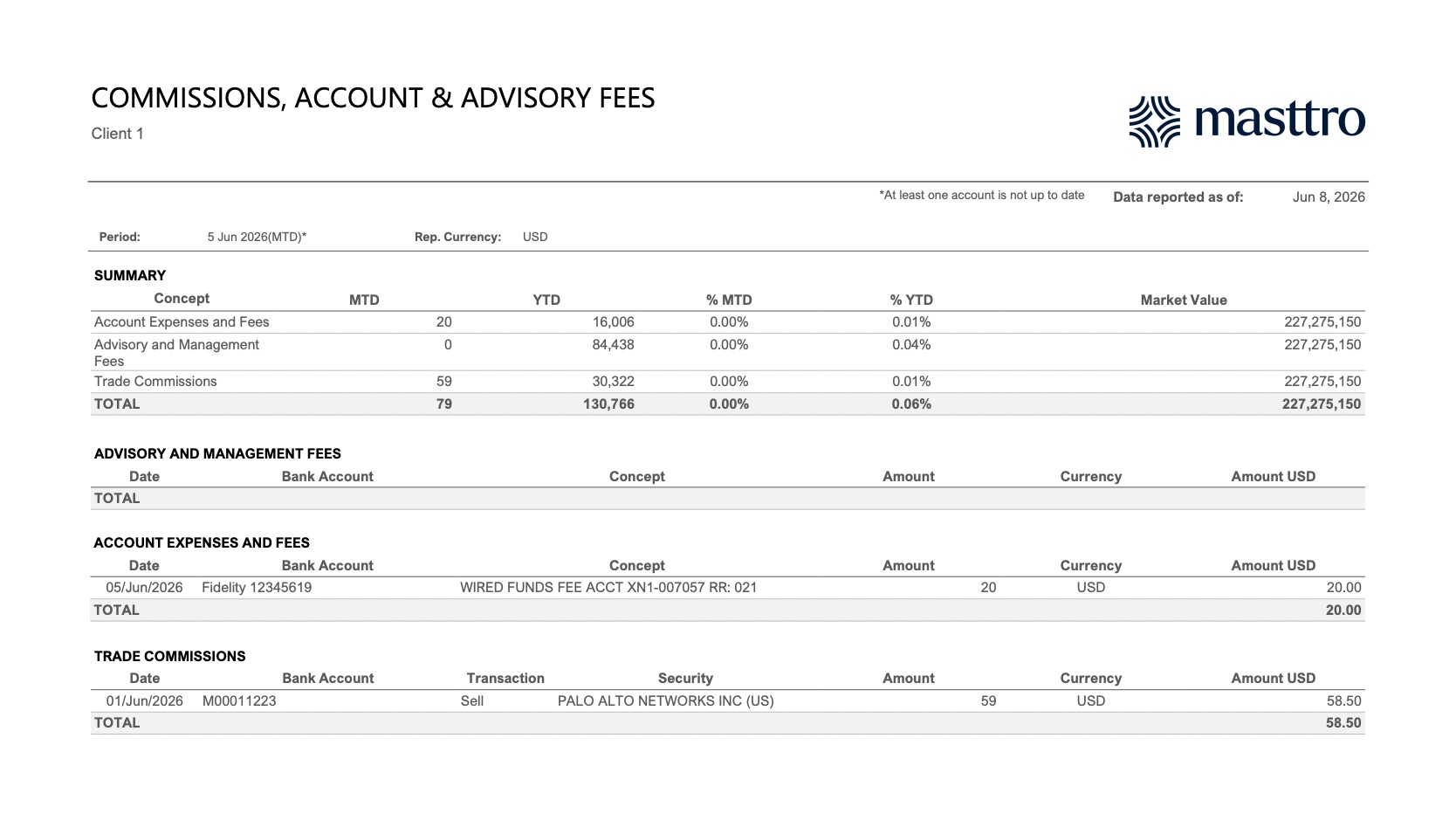

The cost layer answers a question most cash reports ignore: what is our cash actually paying out to operate? Use it to capture trade commissions, account expenses, custodian wire fees, and advisory and management fees. Summarize all costs month-to-date and year-to-date, and break them down by custodian so that cost leakage becomes visible against the portfolio’s market value.

The average family office costs roughly 0.35% to 0.44% of assets to run (UBS Global Family Office Report 2025), a meaningful share of which flows straight out of cash accounts.

Two reports carry this layer.

- A trade-commission-and-account-fees summary aggregates commissions and fees by custodian alongside each custodian’s market value and trade volume. This is useful for spotting which relationships are expensive relative to the value of the assets they hold.

- A consolidated commissions, account, and advisory fees report then splits the total into advisory and management fees, account expenses, and trade commissions, with month-to-date and year-to-date columns expressed as basis points of market value.

Read together, they turn a scatter of small debits (a $20 wire fee here, a $59 trade commission there) into a clear annual cost picture for the wealth owner. Cost visibility has a strategic dimension too: advisors increasingly frame disciplined cash and fee management as a source of value creation rather than mere housekeeping (EY, 2025).

What are the biggest cash flow tracking challenges?

The biggest challenges are structural: fragmented custodian data, manual aggregation, capital-call obligations that sit off the balance sheet, sweep accounts that hide real balances, and multi-currency noise. Together they leave the cash view stale and backward-looking.

Reporting from spreadsheets compounds the problem: each new custodian, entity, or commitment added on top of a manual foundation increases the risk that the consolidated number is wrong.

The single most dangerous blind spot is the capital-call obligation. It is committed but undrawn, so a backward-looking cash report shows a perfectly healthy balance right up until the call lands, at which point the office may have to sell a liquid position at a disadvantageous price or draw on an expensive line of credit.

Sweep accounts create a quieter version of the same problem: cash swept into a money-market fund can read as “invested” rather than “available,” obscuring the firm’s true liquidity. Intercompany loans also distort the consolidated view in the opposite direction, double-counting cash that is really an obligation between entities. And currency translation can move the apparent consolidated balance by several percentage points from week to week, rendering suspect any report without a clear FX-rate-as-of timestamp.

How does technology consolidate cash flow across custodians, entities, and currencies?

Modern platforms consolidate cash flow by aggregating every custodian feed into one normalized ledger, classifying each transaction by type, translating every balance into a single reporting currency, and projecting future flows automatically. This replaces the manual stitch-together with a live view that updates as data arrives.

Four capabilities matter most:

- Automated multi-custodian aggregation pulls in every feed and applies consistent transaction classification, so a dividend, a capital call, and a wire fee are tagged the same way regardless of which custodian reported them.

- A cash management registry acts as the single source of truth for balances across every account and entity.

- Document processing reads incoming capital-call notices and posts them to the forecast automatically, closing the off-balance-sheet blind spot described above.

- Real-time, multi-currency consolidation means the principal sees one figure in the reporting currency while the controller retains the native-currency detail underneath.

Explore how this works in practice with Masttro’s cash management registry and the broader family office reporting software overview.

How do you choose a cash flow reporting platform?

Ensure the family office platform can cover these five dimensions:

- Aggregation coverage: does the platform connect to your actual custodians and banks, or does it rely on a third-party aggregator or data scraper?

- Transaction classification: can it tag and normalize every cash event accurately across feeds?

- Forward projection and capital-call workflow: does it produce both summary and per-security projections, and parse capital-call notices, out of the box?

- Multi-entity and multi-currency consolidation: can it roll up trusts, LLCs, and foundations across currencies while preserving native detail?

- Report-library depth: does it produce the actuals, projection, and cost reports covered in this guide?

With family office assets projected to climb from roughly $3.1 trillion to $5.4 trillion by 2030 (Deloitte Family Office Insights Series), the cost of a backward-looking, manual process is only going to compound.

A simple buyer’s test maps each cash-flow question to the report a platform must produce:

What moved requires a transaction and cash flow ledger plus a reconciled cash ledger.

What’s coming requires summary and detailed projection reports with a capital-call workflow.

What it cost requires fee and commission reporting by custodian.

A platform that cannot produce all three layers leaves the firm dependent on spreadsheets or itger underpowered tools. For a structured comparison of the category, see the best wealth management reporting software.

FAQs

What is cash flow management for a family office?

Cash flow management for a family office is the practice of recording, consolidating, and projecting all cash movements across every account, custodian, entity, and currency, so the office always knows its current balances, upcoming obligations, and the cost of running the portfolio. Cash funds every capital call, tax payment, and distribution, so managing it accurately is a balance-sheet function rather than a clerical one.

Which reports does a family office need to track cash flow?

A complete set spans three layers. The actuals layer includes a transaction and cash flow report, a focused cash flow report, a cash ledger with running balances, a transfers in/out report, and an income report. The projection layer includes a cash projection summary and a detailed per-security projection. The cost layer includes a trade-commission-and-account-fees summary and a consolidated commissions, account, and advisory fees report. Each answers a different question: what moved, what’s coming, and what it cost.

What is the difference between a cash flow report and a cash ledger?

A cash flow report summarizes income, expense, and deposit/withdrawal activity for a period and nets to a single total. It answers what your operating cash movement was. A cash ledger shows a running balance after each transaction, per account, in both local and reporting currency. The ledger is the reconciliation backbone that proves the consolidated cash figure is correct, while the cash flow report is the period summary built on top of it.

How do family offices forecast future cash flow and capital calls?

Family offices model expected inflows (coupons, dividends, maturities, and fund distributions) against expected outflows (capital calls, loan amortizations, and operating and lifestyle costs) across a rolling 12 months, producing a net cash flow and ending balance for each month. They reserve cash against probability-weighted future capital calls rather than waiting for notices. With 32% of family offices planning more private credit in 2025-2026 (BlackRock 2025), call-timing accuracy is increasingly important.

Why is cash flow harder to track when a family office holds private-market assets?

Private-market funds draw and distribute cash on their own timelines, so capital-call obligations sit off the balance sheet and never appear on a normal statement. A backward-looking report can show a healthy balance right until a call lands. Alternatives are now 42% of family office portfolios (BlackRock 2025), so these unpredictable flows now make up a large share of total cash activity.

How does technology improve family office cash flow tracking?

Platforms aggregate every custodian feed into one normalized, multi-currency ledger, classify each transaction, and project future flows automatically, replacing manual spreadsheet aggregation with a live, reconciled view. They can also parse capital-call notices and post them to the forecast, closing the off-balance-sheet blind spot.

How often should a family office report on cash flow?

Billion-dollar offices should track actuals daily, refresh forward projections at least weekly, and stress-test the ending balance monthly against large or early capital calls. Quarterly cash reporting is no longer adequate when calls fire on 5 business days’ notice and tax payments fall on quarterly schedules. The reporting cadence should match the speed at which obligations can arrive, not the convenience of the spreadsheet that produces it.

How is cash flow tracking different from liquidity reporting?

Cash flow tracking is the underlying record: the transactions, projections, and costs that show how cash actually moves. Liquidity reporting is the analysis layer on top, measuring whether the family can meet obligations through metrics like coverage ratios and days-to-cash. You cannot produce reliable liquidity metrics without accurate cash flow tracking underneath, which is why the report set covered here is the foundation rather than the finished product.