Private equity now sits at 21% of average family office AUM, the largest single alternative allocation (UBS Global Family Office Report 2025). And if you're like most family offices, you're tracking that exposure in a spreadsheet that's already out of date.

If that stings a little, you're in good company. Most family offices reconciling capital calls, commitments, and NAVs across 20-plus GPs are doing it by hand, in tabs that break the moment a fund sends a restated statement. So you go searching for "private equity portfolio monitoring software," and page one fills up with tools built for general partners watching their own portfolio companies. That's the wrong side of the cap table. None of it answers the question you actually have: what do I own, what's it worth, and what's my real exposure right now?

This guide is built for the limited partner side, and specifically for family offices. We'll cover how to evaluate these platforms as a family office, the specific reports you should demand before signing anything, and how Masttro, Addepar, Arch, FundCount, Canoe, and the rest actually hold up for a family office, not a fund manager.

Key Takeaways

Why family offices need private equity portfolio monitoring software

Family offices now allocate 21% of AUM to private equity on average, the largest single alternative bucket, according to the UBS Global Family Office Report 2025, which surveyed 317 family offices with $1.1 billion average AUM. Even as some offices trim PE this cycle, 39% plan to raise their allocation over the next 12 months (Goldman Sachs, 2025). And 73% of family offices cite private-market data as their single biggest technology challenge (Simple 2025 Family Office Software & Technology Report).

The gap between allocation size and reporting maturity is the problem this category exists to solve.

Spreadsheets break at scale, and they break in three specific ways.

- Volume is the first. A single PE allocation produces a commitment letter, side letter, K-1, multiple capital-call notices, multiple distributions, and quarterly NAV statements per year, so 20 funds means 200+ documents annually, each in a different format.

- Timing is the second. PE NAVs typically lag 45 to 75 days after quarter-end, and many LPs carry an additional one-quarter lag before that data lands in their own reported financials, turning routine reporting into a six-month-old picture if it is not actively chased.

- The entity layer is the third. Most family offices hold PE through multiple trusts, holding LLCs, or feeder vehicles, so each fund position has to be split across several legal entities, then rolled back up for the principal's view.

The hidden cost is not the reporting time itself. It is the reconciliation errors that surface at audit, the missed capital-call windows that strain GP relationships, and the principal who is making allocation decisions on a six-month-old view of the largest alternative bucket in the portfolio. This is now a board-level technology decision, not an Ops project.

The GP vs LP fork: why one search term means two products

“PE portfolio monitoring software” splits into two distinct product categories that share a name but solve different jobs. GP-side platforms, Allvue, Chronograph, 73 Strings, Cobalt (a FactSet company), and CEPRES, help fund managers track the operating performance, valuations, and ESG metrics of the companies inside their fund. LP-side platforms, Masttro, Addepar, Arch, Canoe Intelligence, and FundCount, help limited partners track their commitments, capital calls, distributions, NAV updates, and cross-fund look-through exposure across many GPs.

Most family-office demand sits on the LP side, where private equity at 21% of average AUM (UBS Global Family Office Report 2025) is now too large a bucket to administer by hand.

There is a 60-second test that tells you which side a vendor is on. Open the vendor’s homepage and read the hero headline. If it talks about “portfolio companies,” “value creation,” “operating partners,” or “deal-team productivity,” it is GP-side. If it talks about “commitments,” “capital calls,” “K-1s,” “distributions,” or “look-through,” it is LP-side. The vendors do not always say which is which. Many use generic “portfolio monitoring” language that obscures the split.

Family offices almost always need LP-side functionality first. Some families with significant direct-investment programs also need GP-side tooling for the companies they actively monitor, but that is a second-order need, not the entry point. Buying a GP-side platform for an LP use case is the single most expensive mistake we see family offices make in this category. The platform looks impressive in a demo, then arrives at the family office and cannot ingest a single K-1.

What family offices actually need to monitor

Family offices need software that handles five capabilities. The first three are table-stakes, and are offered by most platforms. The fourth and fifth are where certain platforms diverge.

1. Capital call intake and processing

The single highest-volume PE operational task for a family office. Each GP issues capital calls in its own format with its own terminology, and investors typically have 10 to 14 days to transfer funds after a notice arrives (Masttro analysis of capital call processing). A 20-fund book means a near-continuous stream of inbound notices, each requiring extraction of amount, due date, wire instructions, and remaining commitment.

2. K-1 and NAV statement extraction across inconsistent GP formats

No two GPs format their K-1 or NAV statement the same way. Manual re-keying is where reconciliation errors are born. Document automation, whether through AI-powered extraction or template-based parsing, is the single biggest productivity unlock in the category.

3. Commitment vs called vs distributed tracking

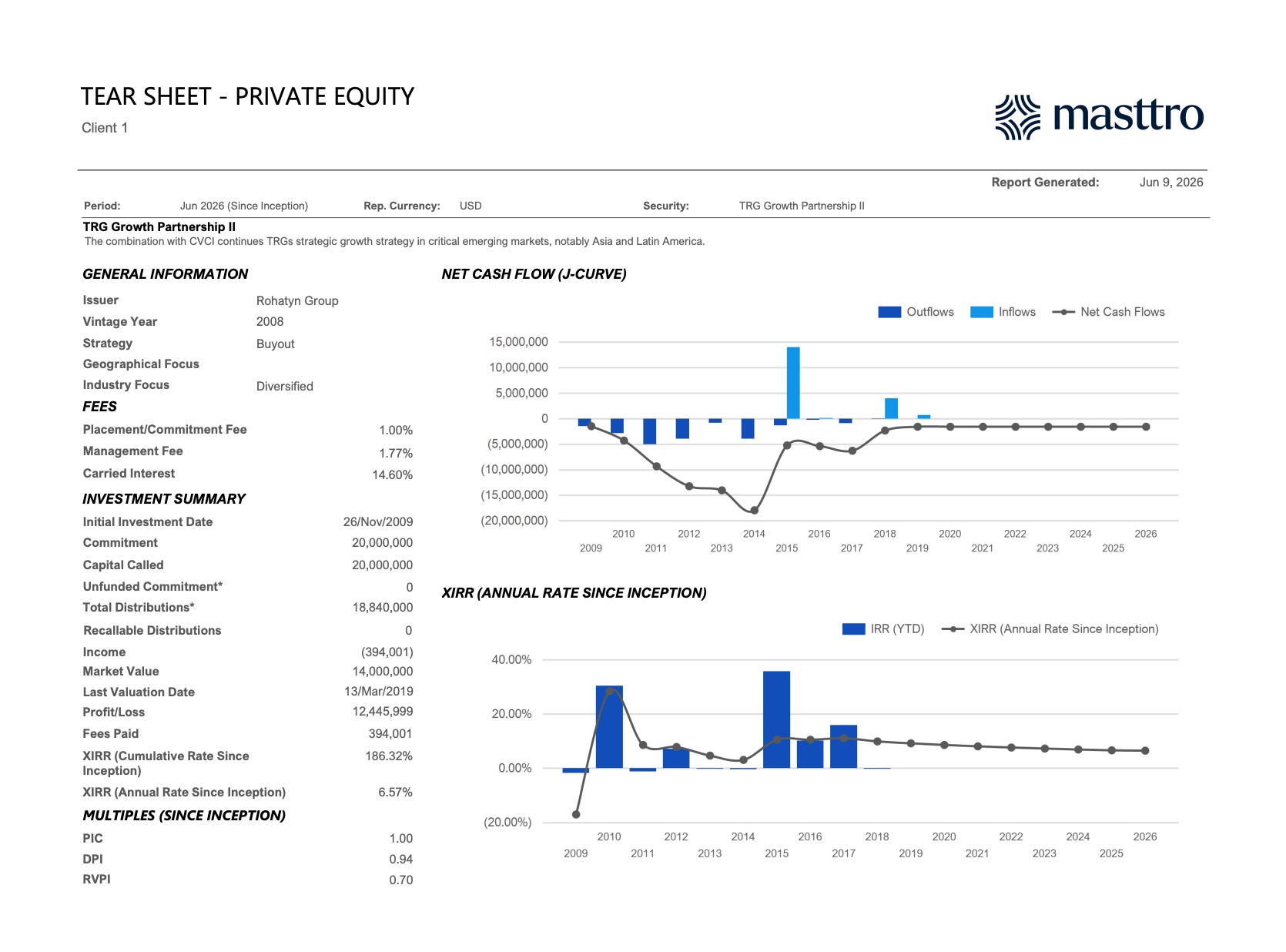

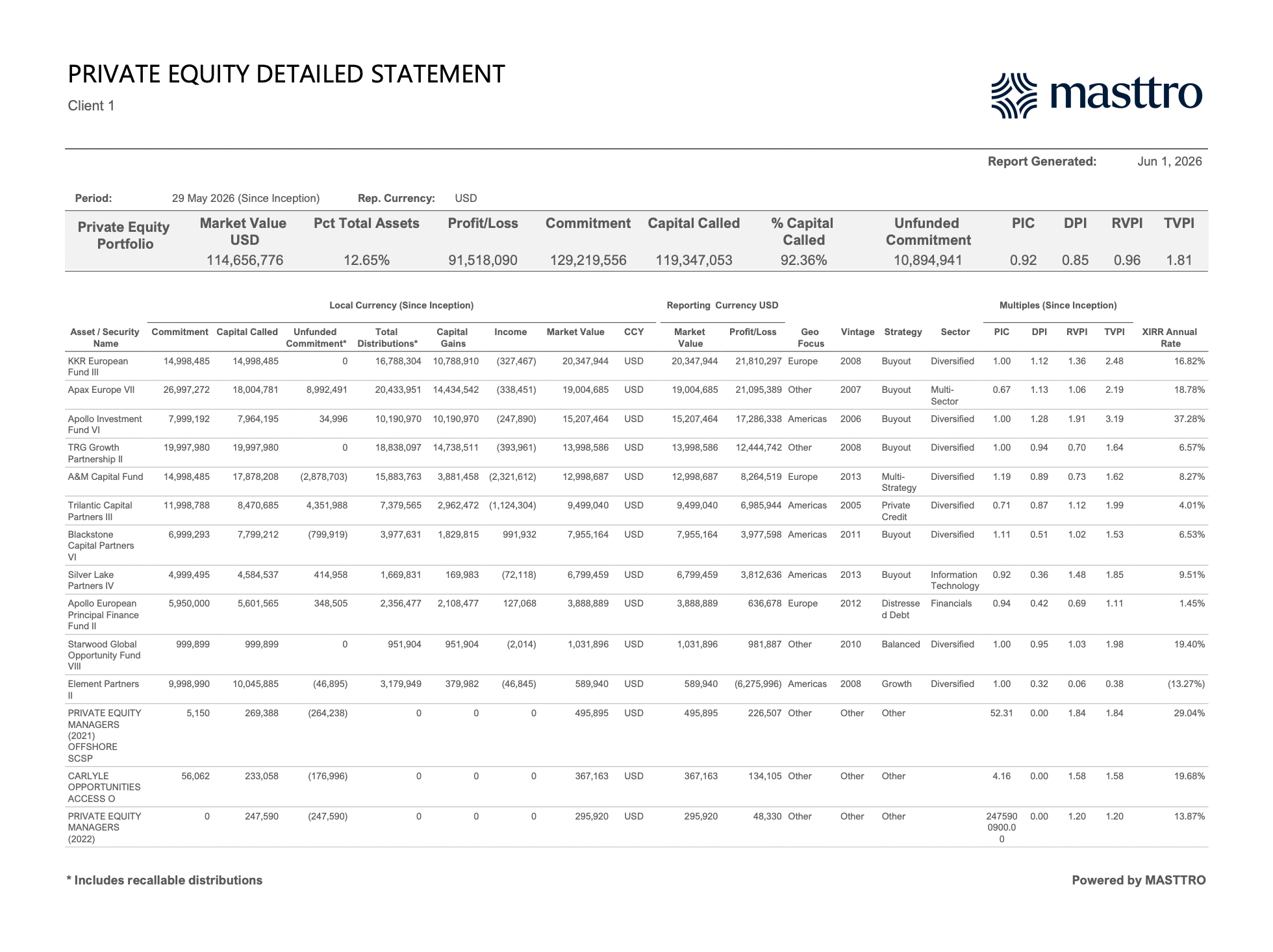

The basic register every family office needs: by fund, by vintage, and by family member or entity. What was committed, what has been called, what has been distributed, what remains. Sounds simple. In a spreadsheet it is one of the most error-prone records a family office maintains. The view above shows what the structured version looks like: every fund line carries its commitment, capital called, unfunded commitment, total distributions, market value, and the multiples (PIC, DPI, RVPI, TVPI, XIRR) computed from the underlying flows rather than typed in.

4. Look-through to underlying holdings

For fund-of-funds, feeder structures, and SPVs, family offices need to see the underlying companies and assets, with proportional allocation back to the family. Without look-through, an entire PE allocation is opaque at the holding level, auditors and family principals cannot interrogate exposure.

5. Integration with the wider wealth platform

PE data that lives in a silo recreates the spreadsheet problem in two systems instead of one. The family office needs PE positions to roll up alongside public markets, real estate, direct holdings, cash, and trusts in a single canonical position.

The PwC and Masttro joint session, “From Chaos to Clarity: Mastering Private Equity Data with Masttro,” walks through what each capability looks like in practice. It is the cleanest public reference for the operational lift family offices experience when they move off spreadsheets.

Best private equity portfolio monitoring software for family offices in 2026

The strongest LP-side platforms for family offices in 2026 are Masttro (purpose-built for family offices, deepest alternatives coverage), Addepar (incumbent, strong reporting, lighter on raw alternatives ingest), Arch (alts-only operations layer for LPs), Canoe Intelligence (document automation specialist, requires a separate reporting layer), and FundCount (full accounting system-of-record). For GP-side direct-investment monitoring, a smaller use case for most family offices, Allvue, Chronograph, 73 Strings, Cobalt, and CEPRES are the category leaders.

39% of family offices plan to raise their allocations to private equity in the next 12 months (Goldman Sachs, 2025). For these families, their software has to scale with a bigger book. The right answer depends on three things: where the family already lives in the wealth-tech stack, how much of the operational lift the team wants to absorb internally, and whether alternatives are a meaningful share of allocation (>20%) or a marginal one.

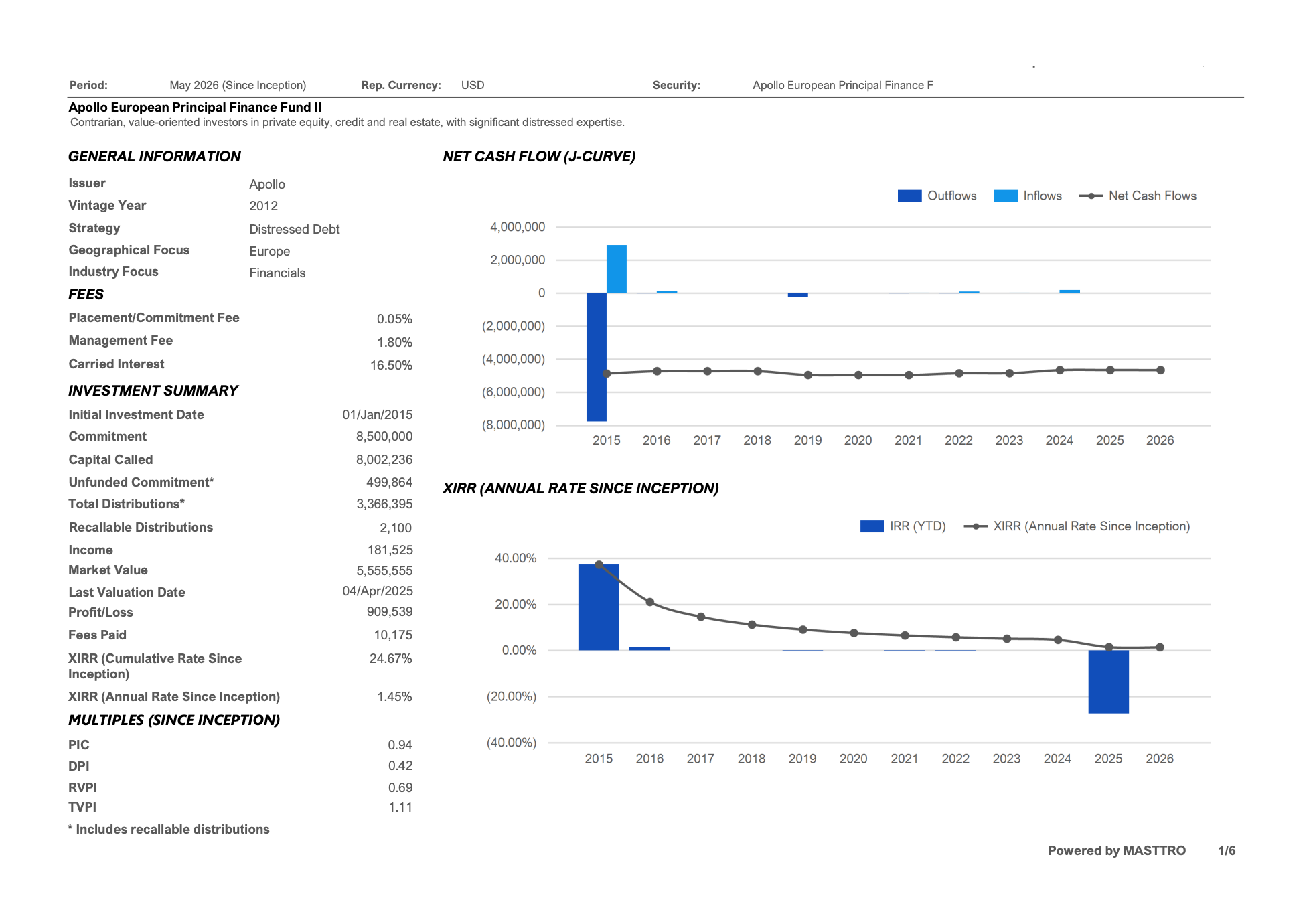

The screen above is the proof point family-office buyers should ask for in any demo: a single-fund deep-dive with the J-curve plotted from real cash flows, the IRR trajectory year over year, the negotiated fees (placement, management, carried interest) surfaced where the operator works, and every multiple computed from underlying data rather than typed in. A platform that cannot produce this view per fund, for every fund the family holds, is not LP-grade.

Masttro vs Addepar for PE portfolio monitoring

Masttro and Addepar both offer LP-side PE monitoring, but the lineage is different and the lineage shows. Masttro was built inside a multigenerational family office in 2010 and grew up handling the full wealth picture, alternatives, real estate, custodians, trusts, lifestyle assets, from day one. Addepar started as an RIA-grade performance and reporting platform and added family-office and alternatives capabilities later. That difference shows up in how each handles raw alternatives document ingestion, the depth of the entity-and-trust data model, and the speed of onboarding for a family with 20+ GP relationships. Masttro goes live in 12 to 14 weeks and runs without a dedicated specialist. Addepar is typically operated by a small group of power users, and many clients carry managed-service contracts that run into five figures a year just to keep the platform running.

Masttro vs Arch vs Canoe (the LP-side alts stack)

Arch and Canoe are alts-only layers. They handle the data work but do not replace the wealth platform that holds the canonical position. Masttro covers both the alts layer and the wealth platform in one system.

73% of family offices name private-market data their single biggest technology challenge (Simple 2025 Family Office Software & Technology Report), so the question is rarely whether the family needs better alts ingestion, only whether to buy it as a layer or get it inside the wealth platform.

When to consider FundCount or a GP-side platform instead

FundCount is the right answer when the family office runs primarily on a true accounting system of record, with multi-entity partnership accounting and a full investor portal as the central requirement. Consider GP-side platforms (Allvue, Chronograph, 73 Strings) only when the family office is also operating direct PE deals at scale with portfolio companies they actively monitor, KPIs, operational metrics, value-creation plans. That is a real but narrower use case. Most family offices with direct deals run a hybrid setup: Masttro for the wealth picture, and a GP-side tool layered on for the active direct holdings.

Alternatives Reporting: From Below the Line to All of the Above

How to evaluate a PE portfolio monitoring platform

Evaluate platforms against six dimensions in priority order for family offices: alternatives coverage depth, capital-call automation, look-through reporting, integration with wider wealth data, implementation timeline, and pricing predictability. Weight the first three at roughly 60% of the decision, as they directly determine whether the platform replaces the current spreadsheet workflow or just digitizes it.

Roughly 75% of family offices report internal expertise gaps in private-market analytics (Simple 2025 Family Office Software & Technology Report). That makes vendor onboarding speed and platform usability decisive evaluation criteria. A platform that requires a dedicated specialist to run is a platform the family office cannot staff.

The demo questions that separate Masttro from everyone else

Most vendors can show you a dashboard. Far fewer can show you how the data got there, what the platform does with it, and what it looks like when your whole world is on one screen. Ask these, and ask to see each one live.

1. Document automation:

"Can you show me how you'd handle a GP capital-account statement, walk me through how a capital call or distribution notice actually becomes data in here?"

Private equity runs on quarterly PDFs, capital calls, distribution notices, capital-account statements, and that's where most platforms quietly fall back on manual entry. Ask your vendor to show the path from a real GP statement to structured, reconciled data, and you'll see document automation that's built for the formats PE actually sends.

2. Alternatives AI

"When that statement comes in, how does the system know the numbers are right? Show me how it reads called vs. uncalled capital and computes the performance figures."

Capturing a NAV is easy; trusting it is the hard part. Ask to see how the vendor’s AI reads a capital-account statement, separates commitment / called / uncalled / distributed, computes the PE performance metrics, and flags anything that doesn't reconcile against the prior quarter. That's the difference between a system that stores PE data and one that actually understands it.

3. Masttro Intelligence

"Across my whole PE book, what would the platform flag for me, without me building a report? Upcoming calls, where I'm concentrated, anything off?"

A storage tool answers "what funds do I own?" An intelligence layer answers "what should I be watching this quarter?" Ask Masttro to surface upcoming capital calls, concentration by GP or vintage year, and performance outliers across the portfolio, unprompted. That shift, from data warehouse to decision support, is what Masttro Intelligence delivers.

4. Global Wealth Map

"Now show me where private equity actually sits in the bigger picture, across every entity and currency, and how it traces down to a single family member."

Most platforms show PE in isolation. Ask Masttro to place the private-equity allocation inside the full net-worth view, every entity, currency, and asset class on one screen, with look-through from the top holding down to the individual family member. For a family office, PE monitoring is a consolidation problem, and the Global Wealth Map is built to solve it.

5. The proof screen:

"Can you click into one fund and show me the full statement, DPI, TVPI, the J-curve, all computed from the actual cash flows?"

This is the LP-grade test. Ask Masttro to open a single-fund deep-dive: a line-item Detailed Statement with PIC, DPI, RVPI, TVPI, and XIRR computed from the underlying cash flows, plus a J-curve plotted from the fund's real call-and-distribution history. If a platform can go from the whole-portfolio map down to fund-level flows without exporting to Excel, it's built for private equity.

Capital call automation: the operational test that separates LP-grade platforms

Capital call automation is the single best test of whether a PE portfolio monitoring platform was actually built for LPs. It requires parsing inconsistent GP formats, extracting amount, due date, wire instructions, and remaining commitment, and routing the notice for approval and payment, all without manual re-keying.

Each GP formats their capital call notices differently with different terminology. Some send PDFs with structured headers; some send scanned images with handwritten signatures; some embed the wire instructions inside a side letter rather than the call notice itself. The manual workflow, download from GP portal, rename the file, extract amount and wire details, internal approval routing, payment, reconciliation, recording in the commitment register, commonly consumes 1–3 hours per call. At 20+ active funds with quarter-end clustering, that load becomes unsustainable.

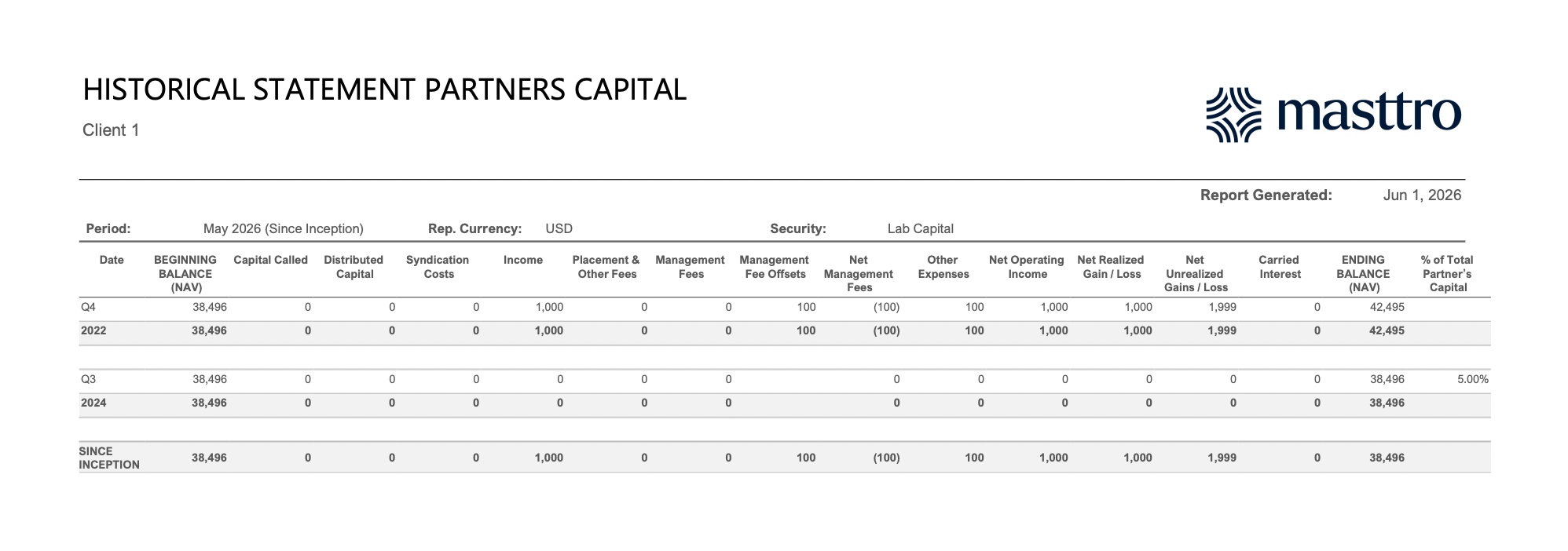

The view above is what proves automation actually worked. The Historical Statement of Partners Capital ties every period’s NAV movement to the underlying capital-call, distribution, fee, and gain/loss line items the GP reports. If a platform automates capital calls but cannot produce a period-by-period partner's capital reconciliation that matches the GP’s statement, the automation is brittle. It parsed the document but did not land the data in the audit trail.

Look-through reporting: why fund-of-funds and feeders break most platforms

Look-through reporting, the ability to see the underlying holdings inside a fund-of-funds or a feeder vehicle, with proportional allocation back to the family, is where the majority of PE portfolio monitoring platforms either do not try or fail silently.

The structures family offices commonly hold, including fund-of-funds, feeder funds, parallel vehicles, and SPVs co-investing alongside the main fund, multiply the look-through depth required to answer a question as simple as “what is our total exposure to this single underlying company?”

Platforms differ along three lines. Full look-through models the underlying holdings, applies proportional allocation, and lets the principal interrogate exposure at the company level. Partial look-through stops at the fund line and asks the user to manually attach an underlying-holdings schedule. No look-through treats the fund as a single line item and is honest about it. The platforms that fail silently are the second category; they appear to support look-through in the demo, then the family discovers at year-end that the underlying schedule is a CSV upload the team has to maintain by hand.

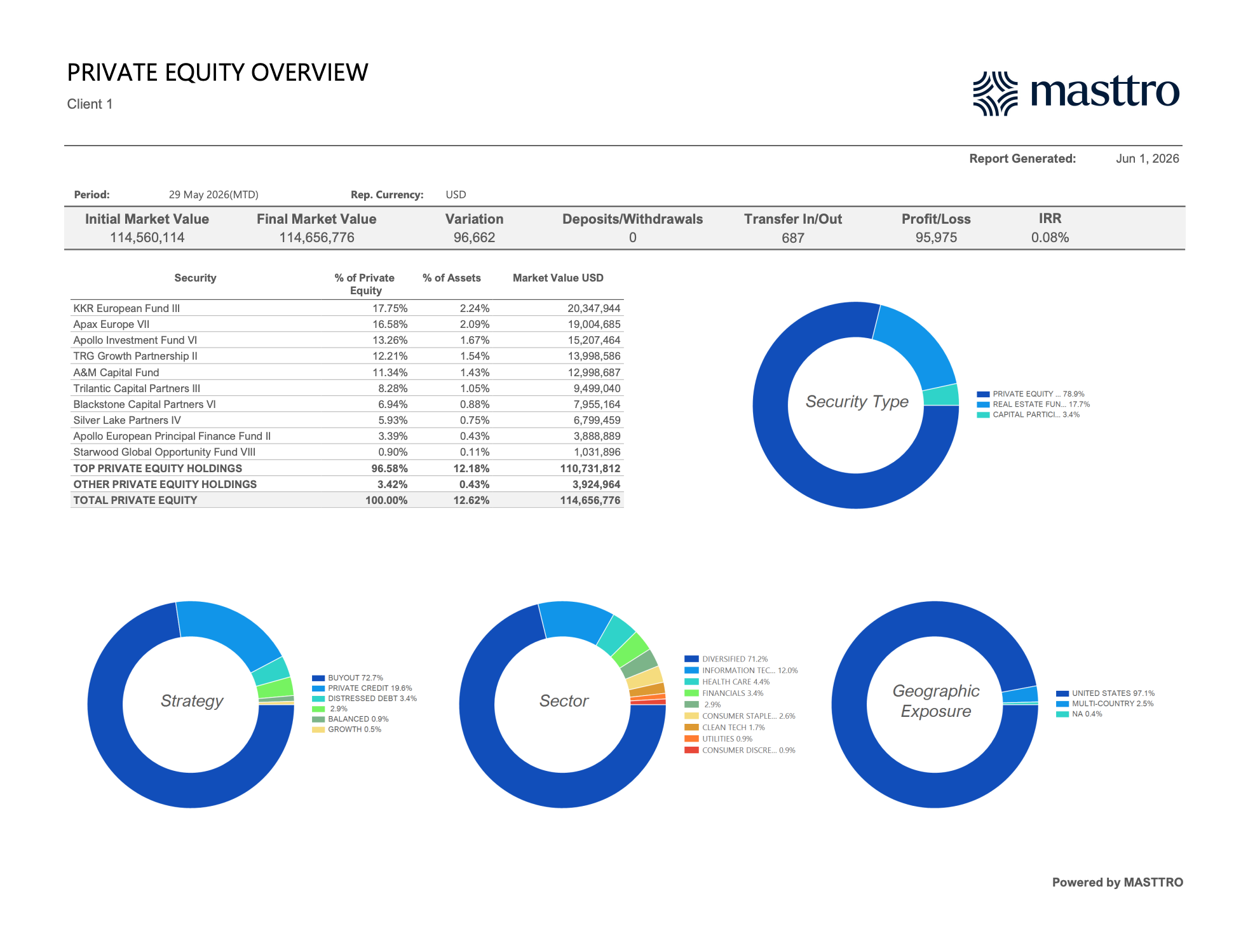

The four exposure donuts on the PE Overview, Security Type, Strategy, Sector, Geographic Exposure, are themselves look-through aggregations. The Strategy donut that shows Buyout 72.7% and Private Credit 19.6% rolls up across funds. The Sector donut that shows Information Tech 12.0% and Health Care 4.4% reaches through fund-of-funds into the underlying portfolio companies. That is the difference between a platform that supports look-through structurally and one that asks the user to maintain underlying-holdings schedules by hand.

Integration: why PE data can’t live in a silo

PE portfolio monitoring software that does not integrate with the family office’s wider wealth data, public markets, real estate, direct holdings, cash, trusts, forces a separate reconciliation workflow and recreates the spreadsheet problem inside two systems instead of one.

Family offices handle data from more than a dozen systems across accounting, banking, portfolio monitoring, and legal, and when those do not sync, workflows fragment and teams revert to manual workarounds (Simple 2025 Family Office Software & Technology Report). Every disconnected tool adds another reconciliation surface, and reconciliation surfaces are where reporting errors are born.

True integration means three things, in order of difficulty. First, a unified data model. PE positions live in the same canonical store as public markets, real estate, and cash, not in a separate sidecar database.

Second, custodian-grade data feeds. These are direct connections to custodians and administrators that are more secure and more reliable than third-party aggregators.

Third, entity-aware ownership and look-through. Any PE position rolls up differently for tax purposes than it does for performance reporting, and the platform needs to know the difference.

The wealth platform owns the canonical position. The PE tool feeds it. The 12.62% number on the PE Overview at the top of this article, Pct Total Assets, is the same 12.62% the principal sees on the family’s consolidated balance sheet. That reconciliation matches because there is only one source of truth, not two systems claiming to be authoritative. Any vendor that proposes the inverse, the PE tool as the canonical store with the wealth platform as a reporting consumer, is selling a tool that solves a smaller problem than the family office actually has. The deeper picture of what that looks like across all asset classes lives in Alternative Investment Reporting for Family Offices.

Implementation, pricing, and the decision framework for 2026

A realistic family office implementation timeline for a PE portfolio monitoring platform is 8 to 16 weeks from contract to first clean NAV close. Pricing typically lands in the $25,000 to $150,000 annual range depending on AUM, fund count, and whether the platform is bundled with a wider wealth solution.

Implementation phases cleanly into three stages: historical data load (4–8 weeks, every existing fund’s commitment, called, distributed, and current NAV history needs to land in the platform), live data feeds (2–4 weeks, custodian connections and GP document workflows go live), and reporting cutover (2–4 weeks, the family transitions away from the legacy spreadsheets).

Pricing models cluster into four shapes.

- Flat subscription (most predictable, common among platforms that do not observe or track client AUM, like Masttro).

- AUM-tiered (most common among incumbents like Addepar. Fees grow with the family’s wealth).

- Per-fund (most common in alts-only specialists like Arch and Canoe).

- Bundled (PE monitoring as part of a wider wealth platform).

96% of family offices reported difficulty recruiting staff in 2025, and 45% reported difficulty retaining it (RBC/Campden Wealth, 2025). That talent constraint makes platform usability and time-to-value the dominant total-cost-of-ownership variables, not license fees. A $150,000 platform the team can run with the staff it already has is a better economic outcome than a $50,000 platform that needs a dedicated specialist the family office cannot find.

The decision framework is straightforward. If alternatives are >20% of allocation and growing, prioritize a full-stack LP wealth platform that handles alts ingest natively. If alternatives are <10% and the family already runs on a strong wealth platform, layer in document automation rather than replacing the system of record. If the family is running direct PE deals at scale alongside fund commitments, plan for a hybrid setup, wealth platform plus GP-side tooling for the active direct holdings.

The platform you choose now has to scale with a bigger PE book. That’s the design constraint that many UHNW families are contending with in 2026.

FAQs

What is private equity portfolio monitoring software?

Private equity portfolio monitoring software is the system family offices, endowments, and limited partners use to track commitments, capital calls, distributions, NAV updates, and look-through exposure across private fund investments. For LPs it replaces the spreadsheets most family offices still rely on, even as 73% name private-market data their biggest technology challenge (Simple 2025 Family Office Software & Technology Report). Separately, GP-side platforms track portfolio-company KPIs and valuations for fund managers.

How is GP portfolio monitoring software different from LP portfolio monitoring software?

GP-side platforms, Allvue, Chronograph, 73 Strings, Cobalt, CEPRES, help fund managers track the operating performance of the companies inside their fund. LP-side platforms, Masttro, Addepar, Arch, Canoe Intelligence, FundCount, help investors such as family offices and endowments track their commitments across many funds. Family offices almost always need LP-side functionality first. A direct-investment program at scale is the only case where the family also needs GP-side tooling.

How do family offices monitor private equity investments today?

Most family offices still rely on manual methods, including spreadsheets, paper statements, and email-based handoffs, to aggregate PE data, and 73% name private-market data their biggest technology challenge (Simple 2025 Family Office Software & Technology Report). Modern platforms automate capital-call intake, NAV ingest, K-1 extraction, and look-through reporting across many GPs simultaneously. The shift is being driven by private equity now sitting at 21% of average family office AUM (UBS Global Family Office Report 2025), which is too large a bucket to administer by hand.

How long does it take to process a private equity capital call manually?

Investors typically have 10 to 14 days to transfer funds after receiving a capital call notice. The manual workflow, downloading from GP portals, extracting amount and wire details, internal approval, payment, and recording in the commitment register, commonly consumes 1 to 3 hours per call (Masttro analysis of capital call processing). At 20-plus active funds with quarter-end clustering, that load becomes unsustainable, which is the operational pressure driving the move to automation.

What is look-through reporting and why does it matter for PE?

Look-through reporting is the ability to see the underlying holdings inside a fund-of-funds, feeder fund, or SPV, with proportional allocation back to the family. It matters because without it, an entire private equity allocation is opaque at the holding level. Auditors and family principals cannot interrogate exposure, and reporting collapses into trust-me line items. “Show me total exposure to Company X across all our PE positions” is the litmus test a platform either passes in 30 seconds or fails entirely.

How much does private equity portfolio monitoring software cost?

Family-office-grade PE monitoring platforms typically price in the $25,000 to $150,000 annual range depending on AUM, number of funds tracked, and whether the platform is bundled with broader wealth reporting. AUM-tiered pricing is most common among incumbents. Flat-subscription pricing is more common among platforms that do not track client AUM. Total cost of ownership is dominated by internal staff hours rather than license fees, especially given that 96% of family offices reported difficulty recruiting staff in 2025 (RBC/Campden Wealth, 2025).